Findings

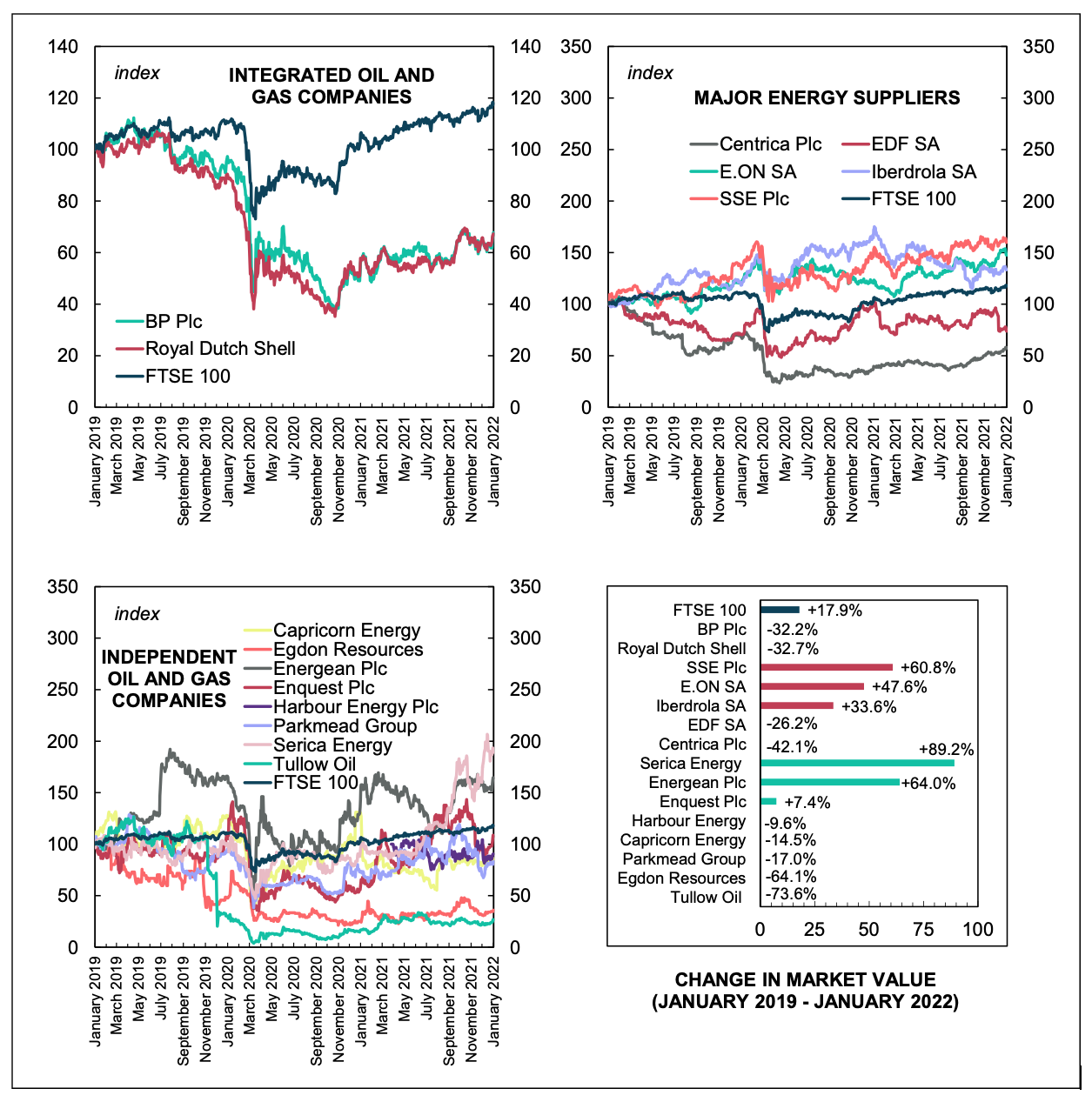

One challenge that we face in tracing the financial fortunes of UK energy companies in recent months is that internal cash flow data are not publicly available and the latest income statements generally pertain to the period leading up to 30th September 2021 at the very latest. The accuracy of recently reported cash flow estimates from Wood Mackenzie will only be determined in the months ahead once firms begin to release their financial reports for the fourth quarter of 2021. In the interim, market capitalisation data are instructive as they tell us what investors’ intersubjective expectations are with respect to the future earnings of the energy firms, adjusted for risk and discounted to net present value. Moreover, these data tell us about the level of companies’ vulnerability to takeover (including, in principle, by the UK Government). With this in mind, Figure 1 tracks the market valuations of the UK energy companies and compares them to the FTSE 100 benchmark.

[.img-caption]Figure 1: The Market Capitalisation of UK Energy Companies, 2019-2021

Source: Datastream through Eikon. Note: Series data are re-based to 1st January 2019 = 100.[.img-caption]

Figure 1 shows that since the end of 2020, the market capitalisation of both BP and Royal Dutch Shell has been on an uptrend, and there has been an upswing in their market value that coincides with the most intense phase of the energy crisis beginning in August 2021. Nonetheless, both BP and Royal Dutch Shell’s market capitalisation has been lagging far behind FTSE 100 over the past three years, and neither company’s market value has recovered to the levels recorded prior to the outbreak of the Covid-19 crisis. Their recent struggles are illustrative of the deep malaise of the oil and gas supermajors. But perhaps the most significant observation to make here is that their market values are closely connected to oil price levels over the past three years – with the two companies’ valuations recovering significantly since the rebound in oil prices in the second half of 2021.

While BP’s and Royal Dutch Shell’s market capitalisation are highly synchronised, the market values of the major energy suppliers over the past three years are varied. Centrica and EDF lag far behind that of the FTSE 100 over the past three years, whereas SSE, Iberdrola and E.ON easily surpass the financial performance of the average FTSE 100 firm. Similar diversity is evident with the independent oil and gas companies: with two outperforming the FTSE 100, and five others underperforming. Our understanding of the financial fortunes of the UK energy companies is enhanced through examining profit margin (net income/revenue) data since the beginning of the 2010s, as presented in Figure 2. The view that BP and Royal Dutch Shell have generally lagged other firms in the FTSE 100 is confirmed in the top-left chart.

However, perhaps most noteworthy is the sudden recovery in their net income-to-sales ratio since the onset of the energy crisis in 2021. This affirms the oil majors’ assertions that theirs is a cyclical business and that the significant profits they are now enjoying offset the massive losses they have experienced in previous periods when oil prices have been much lower, such as during the outbreak of the Covid-19 crisis. Those advocating a windfall tax will need to think of ways of countering potential arguments that a windfall tax for the oil majors is inappropriate because of the cyclical nature of their business. One way of doing so is to emphasise that the integrated oil companies have spent vast sums on shareholder payouts throughout both the “good times” and “the bad” for the oil business – an issue the briefing will turn to shortly.

[.img-caption]Figure 2: The Profit Margins of UK Energy Companies, 2010-2021. Source: Energy company data from Bloomberg Professional. FTSE 100 data from Datastream through Eikon. Note: Profit margins are calculated by dividing net income by revenues. 2022 Q4 data for BP and Royal Dutch Shell are estimates from Bloomberg Professional.[.img-caption]

The major energy suppliers have similarly struggled to record profit margins in excess of the FTSE 100 average over the past decade. Nonetheless, like BP and Royal Dutch Shell, both Centrica and SSE have enjoyed sharp upswings in their profit margins since the onset of the energy crisis. It is interesting to note that, unlike the other major energy suppliers, these two companies are involved in hydrocarbon extraction in the North Sea.

The financial performance of the independent oil and gas companies since 2010 has been woeful. Only Serica Plc stands as an exception. The profit margins of the six others have been consistently negative. In fact, from 2010-20, these five companies collectively recorded total net losses of £6 billion (see data in appendix). Figure 2 indicates that some of these independent firms are staging a recovery amid the energy crisis. Nonetheless, we should be in no doubt that if a windfall tax was only to target oil and gas producers, and not the major energy suppliers or oil trading firms, almost all the tax revenues would come from the integrated oil companies. To put the tiny size of independent oil and gas firms in perspective: the eight included in our analysis have together generated revenues of £32.2 billion since 2010. In contrast, the two integrated oil companies included in our analysis generated revenues of £4.8 trillion in the same period: a sum which is almost 150 times greater.

The strongest case for a windfall tax can be made by emphasising the huge shareholder payouts of BP and Royal Dutch Shell and juxtaposing them with figures regarding their tax payments as illustrated in Table 1. In fact, since 2010, Royal Dutch Shell and BP have together spent an astonishing £147.2 billion on stock buybacks and dividends - far in excess of the FTSE 100 average of £10.8 billion over the same period (see appendix), and over seven times more than the £20 billion that is required to keep households’ energy bills to their current level during this period of elevated wholesale energy prices.

[.img-caption]Table 1: Key Financial Ratios of UK Energy Companies, 2010-2020. Source: Bloomberg Professional.[.img-caption]

Furthermore, as Table 1 shows, since 2010, BP’s shareholder payout commitments have been so large that they cover 98.3% of their pre-tax income, and 2.5 times larger than their tax payments for the period. Thus, even though the effective tax rates of BP and Royal Dutch Shell are greater than that of the average firm in the FTSE 100, their business models clearly generate far greater returns for shareholders than it does for the public coffers. While some of the shareholder payouts will find its way in the hands of the British public via pensions and other investments, the distribution of these proceeds is highly uneven. In fact, as documented in a previous Common Wealth report, the top 10% of the population by income own almost half of all pension wealth in the UK – seven times more than the bottom 50% combined.

Similar observations can be made regarding the major energy suppliers: with a combined total of £42.7 billion spent on dividends and stock buybacks since 2010 (see appendix). Moreover, as Figure 2 shows, like the integrated oil and gas companies, what these firms commit to shareholders far exceeds what they pay in taxes. These corporations are engines of inequality: they do what they can to minimise tax payments to governments, while doing their utmost to maximise returns to investors. Their trenchant opposition to windfall taxes should be understood in this context.

The picture for the independent oil and gas firms is rather different, but equally interesting. As detailed by Table 1, one of these firms has paid no taxes since 2010, while another, which has made tax payments, committed 16.6 times the amount to shareholder payouts. Moreover, there are three other independent oil and gas firms that have gained more from tax benefits than they have lost in tax payments. As Table 2 indicates, these net tax benefits amount to £1.4 billion. It is revealing that the two companies netting the largest tax benefits – Capricorn Energy and Enquest Plc – together spent over £104 million on dividends and stock buybacks since 2010, despite consistently incurring losses during this period.

[.img-caption]Table 2: Net Tax Beneficiaries, 2010-2020. Source: Bloomberg Professional.[.img-caption]

Conclusion

This briefing has sought to put discussions regarding a windfall tax on energy companies within a broader context. It offers several insights:

- Despite recent headlines regarding surging cash flows of integrated oil and gas companies, these firms have underperformed the FTSE 100 over the past ten years. The difficulties experienced by the supermajors are reflective of the oil price environment – with oil prices still below the peak of the last commodity super-cycle that extended from the early 2000s to early 2010s. Therefore, advocates for a windfall tax will have to devise ways of countering the oil and gas industries’ claims that in a cyclical business, they should be able to reap the benefits of rising prices given that they are exposed to falling prices at other times.

- The UK energy sector is highly diverse. While the two supermajors – BP and Royal Dutch Shell – have managed to remain profitable over the past decade, seven of the eight independent oil and gas firms have not. All these companies are several orders of magnitude smaller than BP and Royal Dutch Shell in terms of revenues, and they would therefore likely contribute little in terms of tax payments if a windfall tax was introduced. Nonetheless, the fact that two independent oil and gas firms have spent tens of millions of pounds over the past decade of shareholder payouts, while receiving hundreds of millions of pounds in tax benefits should offer an additional justification for a windfall tax. In this regard, the findings of this briefing may be usefully combined with the insights on fossil fuel subsidies offered by a recent Common Wealth report.

- There is a high level of diversity even among the major energy suppliers. While all five energy utility companies reviewed in this briefing have been profitable since 2010, the two firms that have experienced sharpest increases in their profit margins during the current energy crisis – Centrica Plc and SSE Plc – engage in production operations in the North Sea.

- A compelling narrative in favour of a windfall tax would hinge on juxtaposing the energy companies payouts to investors with their tax payments to government. In the current regulatory environment, all these companies have managed to devote much more resources to the former than the latter. The current regime which favours private financial returns via dividends and stock buybacks over public financial returns via tax payments indirectly promotes inequality and arguably undermines the resiliency of the UK energy sector.

One limitation of this report is that it does not examine the major trading companies that act as key intermediaries in oil markets: Vitol, Glencore, Trafigura, Mercuria and Gunvor. These companies appear to be profiting hugely from the recent energy crisis and are therefore worthy of investigation and scrutiny from policymakers.

Appendix

[.img-caption]Table A1: Key Financial Data for FTSE 100 (£ billion). Source: Datastream through Refinitiv.[.img-caption]

[.img-caption]Table A2: Key Financial Data for Integrated Oil and Gas Companies(£ billion). Source: Bloomberg Professional.[.img-caption]

[.img-caption]Table A3: Key Financial Data for Major Utility Companies(£ billion). Source: Bloomberg Professional. Note: Centrica Plc LTM (last 12 months) data ends 2021 Q2: 30/6/2021. SSE Plc LTM data ends 2021 Q1: 3/31/2021.[.img-caption]

[.img-caption]Table A4: Key Financial Data for Independent Oil and Gas Companies (£ million). Source: Bloomberg Professional.[.img-caption]